Q1. What is the MFF?

The Multiannual Financial Framework (MFF) is a 7 year ‘big picture’ EU spending tool which will last from 2014 to 2020. It details the maximum level (ceilings) of what the EU expects to spend on its priorities to fund new and existing programmes such as Horizon 2020, ERASMUS for All, Connecting Europe Facility and the Common Agricultural Policy. It also ensures the annual EU budget is devised and spent correctly to achieve the best results for all EU taxpayers.

Q2. So, Its a big budget?

Not really. The MFF only sets out the upper limits (ceilings) of what the EU can spend; it doesn’t mean any money can yet be spent. As such, discussions over the MFF are more about politics than economics. Annual EU budgets add the missing specifics, usually at levels below the ceilings.

Q3. Why do we need the MFF?

Beginning in 1988 with Delors 1, multiyear EU funding packages sharpen the EU focus on headline programmes and priorities. For a Union of 27 Member States (soon 28 with Croatia joining on July 1 2013), there needs to be limits and coherence between annual budgets to make sure they are cost-effective and focus on what the EU hopes to achieve. The MFF will run alongside the EU2020 Strategy with shared priorities in the areas of employment, research and innovation, education, social inclusion and climate/energy.

Q4. What’s the process for reaching agreement on the MFF?

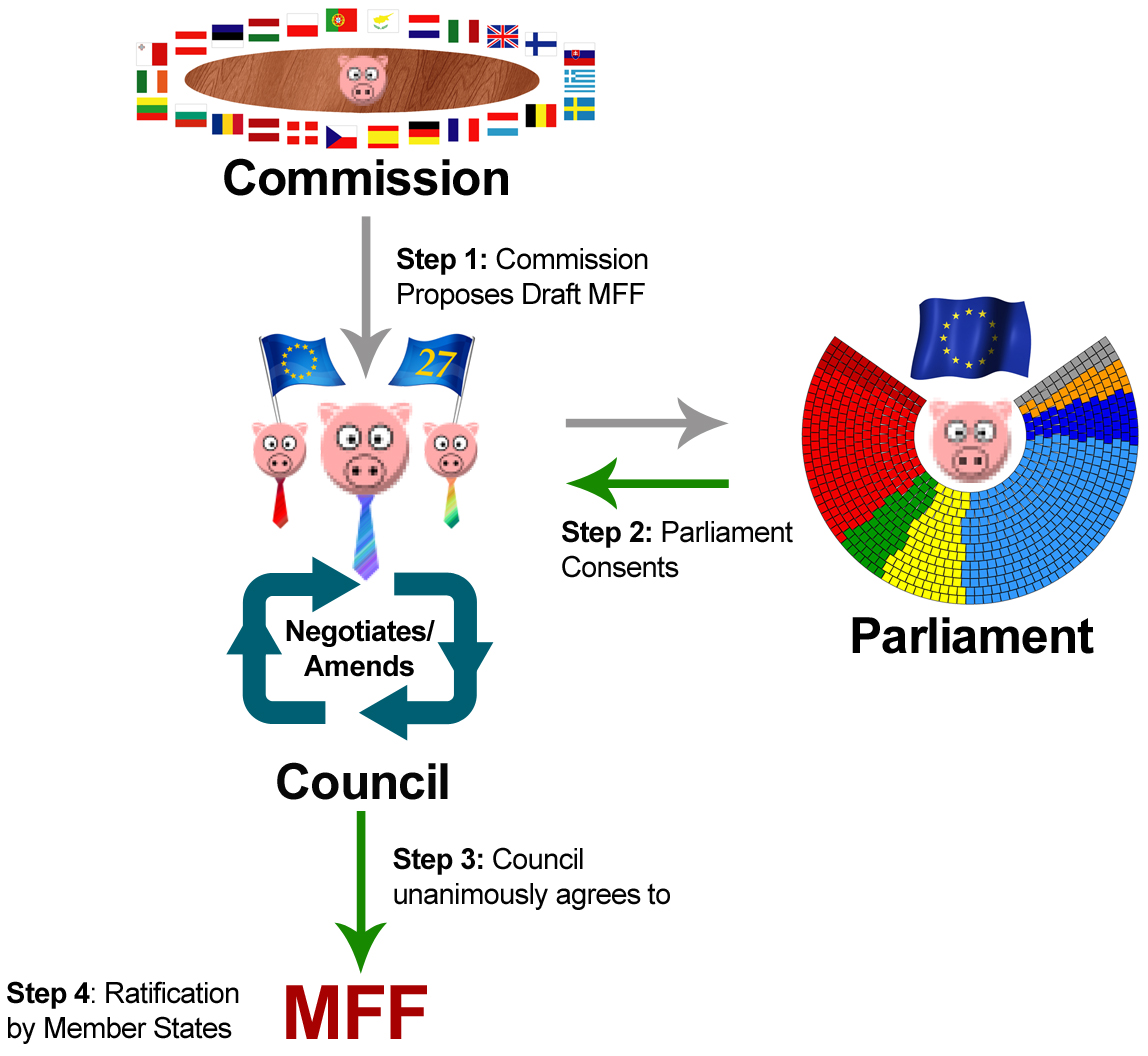

The three main EU institutions have a role in the process; the European Commission, European Parliament and European Council (Heads of State and Government). The Commission proposes while the Parliament and Council work together known as ‘co-decision.’ Roughly speaking, the process is as follows:

The Commission (as the EU executive branch) proposes a package which sets out the terms for negotiation (called a ‘negotiating box’). Discussions take place in the General Affairs Council (GAC) of EU Foreign Affairs ministers where Member States make their views known.

The proposal must first be passed by the European Parliament before being unanimously agreed by the Council (EU Heads of State and Government). Due to the requirement for unanimity, Member States through the Council have huge power. Negotiations are led by the permanent President of the Council, Herman Van Rompuy as the real work lay in bridging the gap between Member States to reach collective agreement (reached last week). It will now go to the Parliament for consent.

Q5. I heard agreement wasn’t easy. How come?

In June 2011, the European Commission led by President José Manuel Barroso proposed a €1.025tn MFF but before that could come into force, the Commission, European Parliament and all 27 EU Member States through their Presidents/Prime Ministers (called the European Council) have to work together to achieve agreement on the political side. On the 7th of February/early morning of the 8th – the European Council finally agreed to a slimmed down €960bn MFF. This was not what most Member States, the European Commission or the President of the European Parliament (Martin Schulz MEP) most wanted. It now passes to the European Parliament for consent.

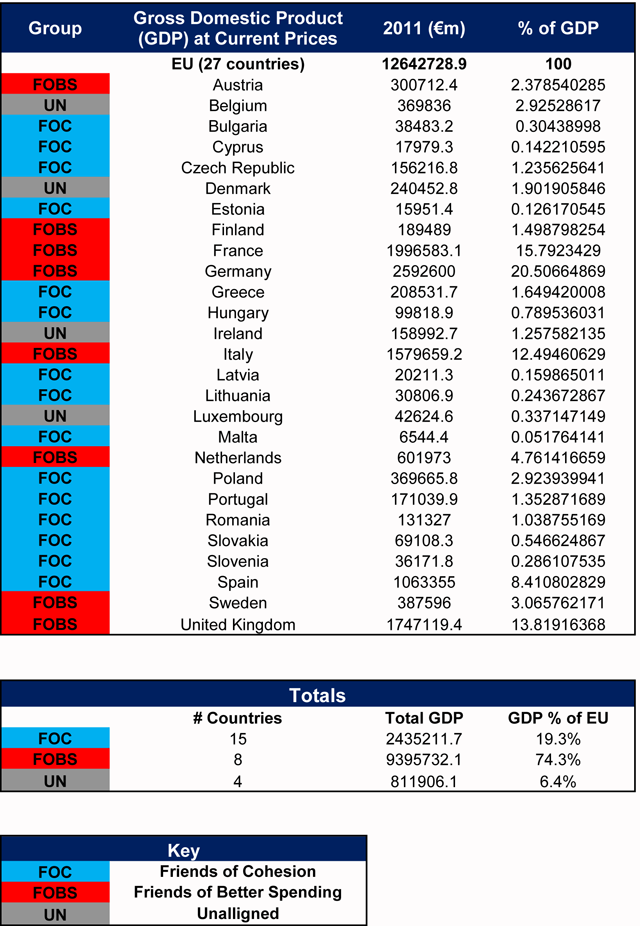

The MFF negotiations were mainly a tug o’ war between those Member States who contribute more than they get back (from benefits from the Single Market or rebates) and those Member States who need EU monies for infrastructural development or to boost their domestic economies . The two groups were as follows:

A. Friends of Cohesion – FOC

Goal: A big MFF with the same/more spending than before

- States which see higher spending as benefiting them most and any reduction in this hurting them in equal measure.

- 15 members mostly those new members who had joined in the 2000s plus Greece, Spain and Portugal.

B. Friends of Better Spending – FOBS

Goal: A targeted, smaller, more efficient MFF

- States who demand restraint and more efficient spending – mainly mature and stable economies.

- 8 members in total.

The FOC had powerful friends in the President of the Commission José Manuel Barroso and European Parliament President Martin Schulz. They preferred the €1.025tn version and met a number of times to confirm/restate their position. The most recent ‘Joint Declaration’ by this group was in October 2012.

This excellent graphic from the European Commission/Financial Times sums up the positions well.

In negotiations, the two opposing camps fought it out. While it might be argued the Friends of Better Spending ‘won’ the argument, the devil is in the detail which is yet to come. Although yes, the Friends of Cohesion have 15 members (of 27), their economies represent only 19.3% of total EU GDP while the ‘Friends of Better Spending’ represent a whopping 74%. The economic argument speaks for itself.

Source: Eurostat

Posted by Editor

Posted by Editor