![]() There has been much debate lately over the Irish economy. Ireland has been held in high esteem across European capitals as somewhat of a poster-child for sticking the bailout conditions laid down by the ‘troika’ (The EU, European Commission, and International Monetary Fund – IMF). This means following a plan to shrink the economy and bring the huge gap between revenue and expenditure closer together. There are, of course, only two levers for a country in monetary union (the euro) to do this – raise taxes and/or cut spending – neither is ever popular buts its same across Europe.

There has been much debate lately over the Irish economy. Ireland has been held in high esteem across European capitals as somewhat of a poster-child for sticking the bailout conditions laid down by the ‘troika’ (The EU, European Commission, and International Monetary Fund – IMF). This means following a plan to shrink the economy and bring the huge gap between revenue and expenditure closer together. There are, of course, only two levers for a country in monetary union (the euro) to do this – raise taxes and/or cut spending – neither is ever popular buts its same across Europe.

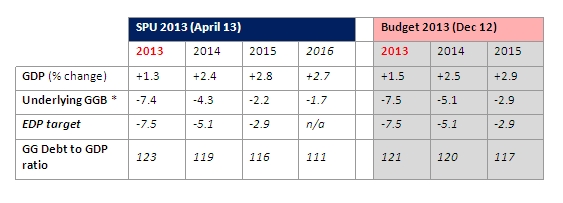

On April 30, the Irish Department of Finance released its report on Ireland’s medium term economic on forecasts called the Stability Programme Update (SPU) which each eurozone country must submit to the European Commission annually as part of the European Semester process (aligning eurozone fiscal policy). The findings were:

Comparison of SPU and Budget 2013 (Presented December ’12)

In summary:

Growth

- The Irish economy is forecast to grow slower (-0.2%) than the original projections at the time of Budget 2013 in December.

Debt

- The general government (GG) debt to GDP ratio (an ideal ‘compliance’ ratio and precondition for joining the euro being 60%), is now projected to stand at 123% this year, falling to 116% by 2015, marginally better than originally predicted in December.

Deficit

- The other Maastricht criterion, that of the ‘excessive deficit procedure’ or EDP is forecast to be -7.5% this year (total revenue less spending), achieving the required level of -3.0% by 2015, as projected in December.

- The approximate €750m – €1bn savings from the ‘prom’ note deal which will knock a good chuck off the cost of servicing the national debt are assumed to help reduce this figure.

- On the positive side, the 2012 figure was -7.6%, well within the EDP target of -8.6%. The Irish economy is now performing at or above expectations in this area and the economy remains on target to hit -3.0% by 2015. Good news and politically valuable breathing space for Finance Minister Noonan as he crafts the next series of budgets. However, successive government ministers insist that austerity is not option and the proposed €3.1bn adjustment required this year under the EU-IMF programme is going ahead in the mid-October budget.

All this is line with the European Fiscal Compact (also known as the Irish Fiscal Stability Treaty) which was ratified by referendum by the Irish people on 31 May by a margin of 6:4. This allowed Brussels to push ahead with more formalised procedures under the Stability and Growth Pact (SGP) to penalise countries which did not follow their commitments and get their finances in order, as was the cost of joining the euro in the first place.

On May 3, the European Commission released their own Spring 2013 Economic Forecast (more here)

The differences between the SPU and the Commission forecast are, notably, slightly more pessimistic than the April 2013 SPU update with a growth project of +1.1% for 2013 rather than the Department’s forecast of +1.3%. But the pessimism is uniform. The Commission forecasts a more rapid decline in the current deficit fueled by the ‘prom’ note deal, a further public sector wage deal with unions (Croke Park II/Haddington Road) and other adjustment measures taking effect from the 2013 budget.

Why the pessimism?

Simply put,weak demand for Irish exports. The continuing uncertainly in the Eurozone with Cyprus, Slovenia and others, coupled with political uncertainties such as the unpopularity of French President Hollande and the federal election in Germany this November. Another issue which could negatively affect exports is the expiry of pharmaceutical patents the so-called pharma patent cliff.

The main issue is that despite the relative buoyancy of exports, there has been no real material recovery in domestic demand. What these forecasts agree on is that 2013 may be the pivotal turning point.

Irish Business Employers’ Confederation (IBEC) Quarterly Forecast

The IBEC quarterly review follows on from the SPU, making particular reference to domestic challenges such as unemployment (stubbornly stuck at 14%), weak consumer confidence and domestic demand and the issue of debt.

But positively, the Irish economic engine appears primed for re-ignition. The only problem is…Europe.

But positively, the Irish economic engine appears primed for re-ignition. The only problem is…Europe.

The key issue is ‘austerity fatigue’ across EU capitals and a renewed emphasis on growth rather than a strict doctrine of austerity. While Ireland appears to be successive, peripherals economies such as Spain, Portugal and Greece remain fragile. IBEC recommends, as ‘we are 85% of the way toward returning the fiscal deficit (EDP) below the 3% limit…the time is now right to ease back somewhat the pace of fiscal adjustment” – the proposed €3.1bn due in the mid-October budget.

Summary of Irish growth prospects

A number of other studies have also forecast Irish growth ahead, summarised here.

On average, Irish growth is therefore forecast at 1.46% (2013) and 2.8% (2014). Far below the ‘Celtic Tiger’ highs of 7%+ but much better than in recent times.

On average, Irish growth is therefore forecast at 1.46% (2013) and 2.8% (2014). Far below the ‘Celtic Tiger’ highs of 7%+ but much better than in recent times.

Read more here.

Posted by Editor

Posted by Editor